Remote Work Before, During, and After…

Why 60% of Foreign Companies Fail

Employer of Record (EoR) and PEO: Where Global Workforce Expansion Is Really Happening

As remote and hybrid work mature into permanent operating models, Employer of Record (EoR) and Professional Employer Organization (PEO) solutions have moved from “tactical hiring tools” to core workforce infrastructure. The post-pandemic period is no longer about whether companies hire internationally, but how fast and where they do so—without triggering permanent establishment (PE), payroll, or labor-law exposure.

The global demand signal: why EoR/PEO adoption keeps accelerating

According to World Bank data, over 70% of multinational SMEs now generate revenue in at least one foreign jurisdiction, yet fewer than 30% maintain legal entities in those markets. This structural gap is exactly where EoR and PEO models thrive.

At the same time, the International Labour Organization estimates that cross-border service employment has grown ~2x faster than goods trade since 2019, driven largely by digital services, technology, finance, and regional HQ functions. The result: strong, sustained demand for compliant employment models that sit between freelancers and full legal incorporation.

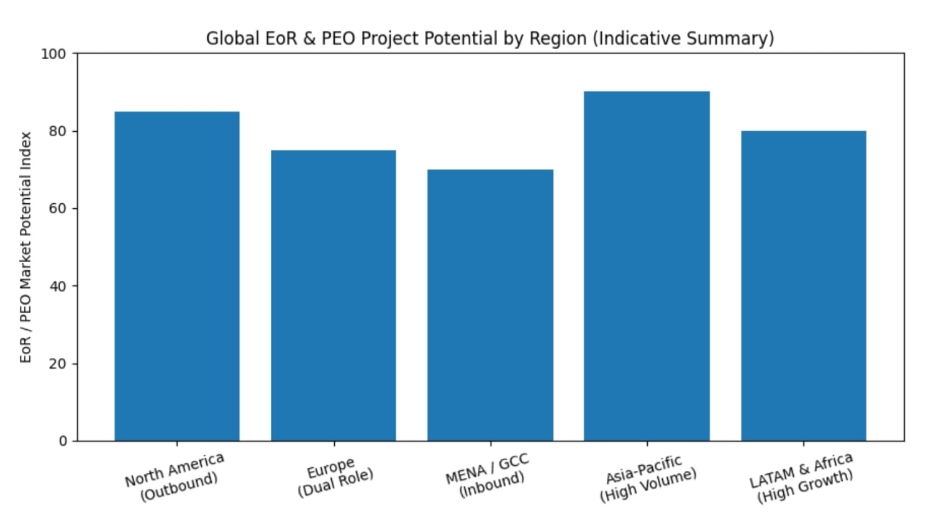

Regional comparison: where EoR and PEO projects scale fastest

North America (US & Canada): outbound demand engine

North America remains the largest outbound EoR market globally. U.S.-based companies account for an estimated 35–40% of global EoR contracts, primarily hiring into:

Europe (engineering, compliance, sales)

LATAM (technology, customer support)

Asia-Pacific (regional operations, cost-efficient talent)

Key driver: speed-to-hire and PE risk mitigation.

Constraint: growing IRS and state-level scrutiny around worker classification and co-employment boundaries, pushing buyers toward mature EoR providers rather than “lightweight” payroll vendors.

Europe: dual role—buyer and supplier

Europe plays a dual role in the EoR/PEO ecosystem:

Outbound: EU startups and scaleups expanding into the US, UK, MENA, and APAC

Inbound: heavy hiring into countries such as Poland, Portugal, Spain, and the Baltics

Eurostat labor mobility data shows that over 20% of EU tech hires in 2023 were cross-border, with EoR being the dominant entry model for the first 5–20 employees per country.

PEO is weaker in Europe due to stricter co-employment and labor leasing rules, making EoR the preferred structure.

MENA & GCC: entity-light expansion hotspot

The Gulf region (UAE, Saudi Arabia, Qatar) is one of the fastest-growing EoR inbound markets, particularly for:

Regional sales teams

Project-based specialists

HQ-lite market entry

Despite business-friendly reputations, entity setup, quotas, and visa compliance still create friction. As a result, EoR adoption in the GCC has grown at ~25% CAGR since 2021, especially among European and Asian companies testing regional presence before full incorporation.

Asia-Pacific: volume-driven, compliance-sensitive

APAC is the largest region by EoR employee headcount, led by:

India

Philippines

Vietnam

Indonesia

Thailand

The driver here is not just remote work, but cost arbitrage combined with regulatory complexity. Local labor laws, social security systems, and termination rules vary significantly, making EoR a lower-risk alternative to DIY payroll.

PEO models are more accepted in parts of APAC than in Europe, particularly where labor leasing frameworks are clearer.

LATAM & Africa: high-growth frontier markets

LATAM and selected African markets represent the highest-growth potential, albeit with higher operational risk:

Currency volatility

Enforcement unpredictability

Rapid regulatory changes

Still, EoR demand in LATAM has been growing 30%+ year-on-year, fueled by nearshoring, time-zone alignment with the US, and deep technical talent pools.

Strategic HR conclusion

EoR and PEO are no longer “temporary fixes.” They are portfolio tools in a modern workforce strategy:

EoR for market entry, compliance insulation, and distributed teams

PEO for scale, cost efficiency, and operational consolidation (where legally viable)

The organizations winning today are those that treat employment structure as a strategic variable, not an afterthought.